In a world where every dollar counts, parking your cash in a traditional savings account just doesn’t cut it anymore. With rising interest rates and increasing financial awareness, high-yield savings accounts (HYSAs) have become the smart saver’s weapon of choice.

But with hundreds of banks and fintechs touting “the best rates in the market,” how do you know where to put your money? This comprehensive guide dives deep into the best high-yield savings accounts in the USA, helping you make a savvy, informed decision—whether you’re saving for a rainy day, a house, or your next adventure.

Why High-Yield Savings Accounts Matter in 2025

In 2025, the average traditional savings account in the U.S. still yields a meager 0.45% APY. Compare that to some HYSAs offering 4.00% to 5.25%+ APY, and the difference is staggering over time.

Let’s do the math:

-

Saving $10,000 at 0.45% APY = $45/year in interest.

-

Saving $10,000 at 5.00% APY = $500/year in interest.

That’s over 10x the earnings — without lifting a finger.

💡 Pro Tip: HYSAs are typically FDIC-insured, so you get both safety and solid returns — the best of both worlds.

What to Look for in a High-Yield Savings Account

Before diving into the top contenders, here’s what makes a high-yield savings account truly great:

1. High APY

The most important factor. Look for APYs of 4.00% or higher in today’s market.

2. No Monthly Fees

Avoid accounts that chip away at your balance with maintenance or service fees.

3. FDIC Insurance

Ensure the bank is FDIC insured (or NCUA for credit unions), protecting up to $250,000 per depositor.

4. Easy Access & Transfers

Online/mobile access, fast ACH transfers, and ATM access (if needed) are key.

5. Minimum Balance Requirements

Some accounts offer high rates only if you meet minimum balance or deposit requirements — read the fine print.

Best High-Yield Savings Accounts in the USA (2025)

Here’s a curated list of the top high-yield savings accounts in the USA, updated for mid-2025.

1. UFB Direct High Yield Savings

-

APY: Up to 5.25%

-

Minimum Balance: $0

-

Fees: None

-

FDIC Insured: Yes (via Axos Bank)

UFB Direct consistently tops the charts with ultra-competitive rates. No account fees, no minimums, and a sleek mobile app make it a winner.

⭐ Best for: Savers who want the highest possible return with no strings attached.

2. SoFi Online Savings

-

APY: Up to 4.60% (with direct deposit)

-

Minimum Balance: None

-

Fees: $0

-

FDIC Insured: Yes

SoFi combines high interest rates with added features like budgeting tools and early paycheck access. Plus, members get perks like financial planning and investing options.

✅ Bonus: Get up to $250 sign-up bonus with qualifying direct deposit.

⭐ Best for: Those who want a full-service financial platform with competitive savings rates.

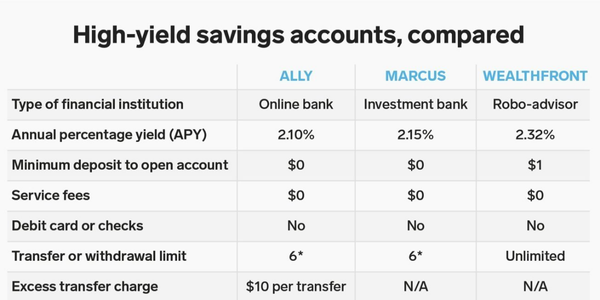

3. Ally Bank Online Savings

-

APY: 4.25%

-

Minimum Balance: $0

-

Fees: None

-

FDIC Insured: Yes

Ally is a well-established online bank known for top-notch customer service and user experience. While the rate is slightly lower than some newcomers, it’s a reliable long-term option.

🔍 Bonus Feature: “Buckets” to organize savings goals (e.g., Emergency Fund, Vacation, Taxes)

⭐ Best for: Budget-conscious savers who value a trusted name and intuitive interface.

4. Marcus by Goldman Sachs

-

APY: 4.40%

-

Minimum Balance: None

-

Fees: $0

-

FDIC Insured: Yes

Marcus offers solid interest rates with the backing of Goldman Sachs. While it’s bare-bones (no checking account), it shines as a pure savings vehicle.

💡 Tip: Use recurring deposits to build momentum without effort.

⭐ Best for: Savers who just want high rates — no frills attached.

5. Discover Online Savings Account

-

APY: 4.30%

-

Minimum Balance: None

-

Fees: No maintenance, excessive withdrawal, or insufficient funds fees.

-

FDIC Insured: Yes

Discover brings its no-fee philosophy to savings. Backed by one of the biggest names in banking, this is a great option for those who already use Discover products.

⭐ Best for: Existing Discover cardholders looking for a seamless ecosystem.

Comparing the Top High-Yield Savings Accounts

| Bank | APY | Minimum Balance | Fees | FDIC Insured | Unique Features |

|---|---|---|---|---|---|

| UFB Direct | 5.25% | $0 | No | Yes | Highest APY, simple interface |

| SoFi | 4.60% | $0 | No | Yes | Bonus perks, full-service suite |

| Ally Bank | 4.25% | $0 | No | Yes | Smart tools, great UX |

| Marcus by Goldman Sachs | 4.40% | $0 | No | Yes | Recurring transfers, easy setup |

| Discover | 4.30% | $0 | No | Yes | No fees across the board |

Real-Life Use Cases: How People Are Using HYSAs Today

💼 John’s Emergency Fund

John, a 35-year-old freelance web developer, keeps $15,000 in an Ally high-yield savings account. He earns over $600/year in interest, all while ensuring quick access in case of unexpected expenses.

🏖️ Maya’s Vacation Savings

Maya automates $250/month into her SoFi savings “bucket” labeled Travel. In just 12 months, she saved $3,000 — and earned an extra $120 in interest for her Bali trip.

🍼 Taylor & Chris’s Baby Fund

Expecting parents Taylor and Chris use UFB Direct for their baby savings fund. At 5.25% APY, their account helps offset rising healthcare and daycare costs.

Tips to Maximize Your High-Yield Savings Strategy

Want to make the most of your savings? Here are a few expert tips:

1. Set Up Auto-Deposits

Treat savings like a recurring bill. Set it and forget it.

2. Label Your Goals

Use account nicknames or buckets to stay motivated.

3. Avoid Temptation

Don’t link your savings account to everyday spending. Out of sight = harder to splurge.

4. Check Rates Quarterly

Rates can change. Review every 3–6 months and switch if necessary.

5. Take Advantage of Bonuses

Many banks offer cash bonuses for new accounts or direct deposits.

Frequently Asked Questions (FAQs)

❓ Are high-yield savings accounts safe?

Yes. As long as your bank is FDIC insured (or NCUA for credit unions), your money is protected up to $250,000 per depositor.

❓ Will my interest rate always stay the same?

No. APYs are variable and can change based on the Federal Reserve and market conditions. That’s why it’s smart to stay informed.

❓ Can I lose money in a HYSA?

Not under normal circumstances. HYSAs are not invested in the stock market — your balance never drops.

❓ How do taxes work on interest earned?

Interest is taxable income. Your bank will send you a 1099-INT form each year.

Final Thoughts: Choosing the Best High-Yield Savings Account for You

There’s no one-size-fits-all answer. The best high-yield savings account depends on your financial habits, goals, and personal preferences. Whether you want maximum APY, digital tools, or a trusted brand, there’s an option on this list for you.

With rates at record highs, now is the perfect time to open a high-yield savings account and start earning passive income on your cash.

💬 What’s Next?

Have you opened a high-yield savings account yet?

Let us know in the comments below, or check out our related guides: